Stop Financial Advisors From Draining Your Parents' Savings

Nov 24, 2024Hello Stoic Investors,

Today, we're going to talk about how to manage and safeguard your parents' retirement investments.

If your parents are over 60 and have investments managed by a financial advisor, you need to read this.

Many advisors don’t prioritize their clients' best interests, which can lead to poor returns and high fees.

One of my students shared a story that highlights this issue.

Her mom, who relied on a financial advisor for 15 years, saw no growth in her investments during one of the stock market's biggest booms.

The advisor charged a 2% annual fee—essentially earning $2,000 a year regardless of performance.

Without any reason to be motivated to make a good result, he would still make this amount!

Financial Advisors Can Easily Take Advantage of Senior Clients

Many financial advisors target older clients due to their limited knowledge about investments.

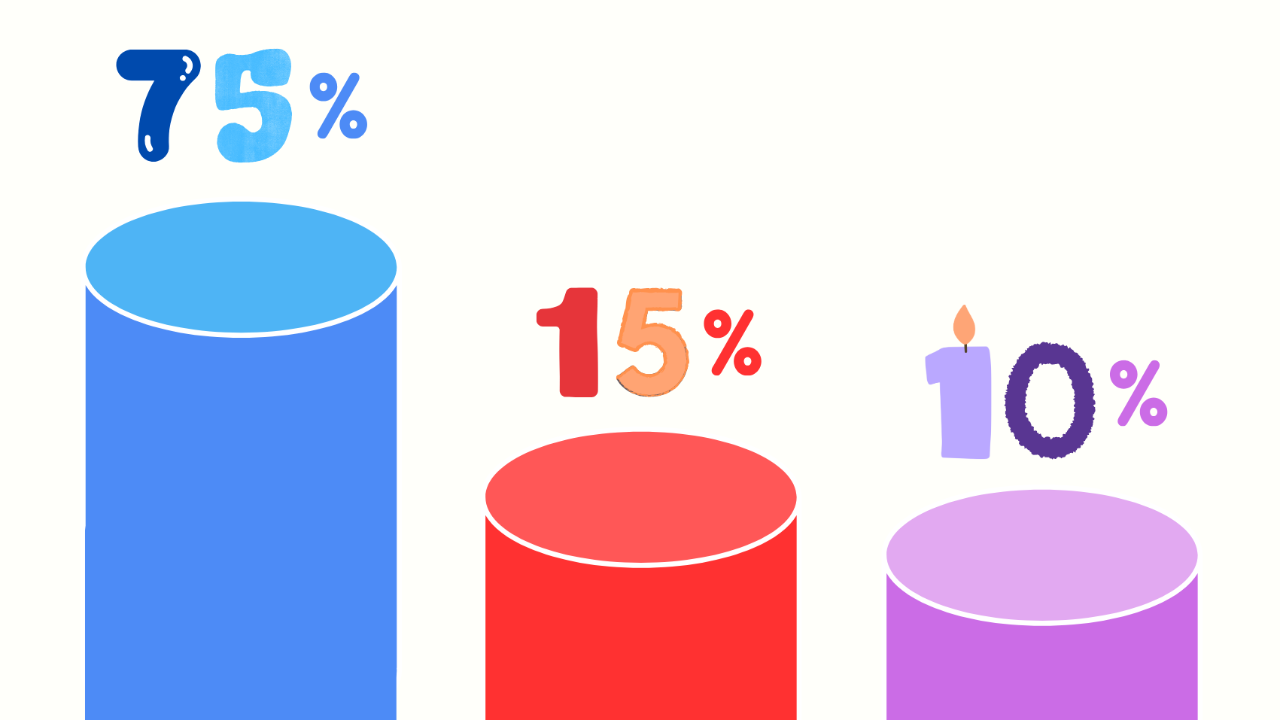

Hidden fees—like entry, exit, and admin fees—can easily erode returns.

A typical setup might include:

2% advisor fee

1-3% fund fees

Additional account or transaction charges

These fees compound quickly, leaving little or no return for clients.

This is why I emphasize learning to invest yourself—only you have your best financial interests at heart.

3 Things You Can Do Right Now to Help Your Parents

1. Review Their Investment Portfolio:

The first step is to sit down with your parents and have a clear look at their investments.

This might be a difficult conversation for some, but it's crucial.

If your parents have various assets, it's important to start talking about these things early on.

Begin by understanding their current financial situation.

Then, compare their investment returns to the general market, like the stock market.

Their returns might be lower, especially if they're older and have a more conservative investment strategy, but they should still be seeing some return, not 0%.

2. Calculate Their Retirement Needs:

Next, figure out how much money your parents will need for their retirement and see if their investments can cover it.

For example, if your parents need $4,000 a month in retirement and $2,000 of that comes from a public pension, then the remaining $2,000 must come from their investments.

Let's say they have $500,000 invested. To get $2,000 a month, or $24,000 a year, from these investments, they would need about a 5% annual return.

This is quite achievable.

This way, they can remain financially secure until the end of their lives, leaving a substantial amount behind for emergencies or inheritance.

3. Set Up Everything to Avoid the Death Tax:

Third, it's important to arrange your parents' finances to minimize inheritance or death taxes.

In many countries, especially in the European Union, assets are taxed when someone passes away.

Instead of waiting until the last moment, consider making arrangements in advance.

This could involve making donations, transferring certain assets, and planning who will inherit properties or investment portfolios.

Taking these steps early is crucial.

For example, in some countries like Belgium, the death tax can be as high as 40%.

This means if your parents have $500,000 in investments, $200,000 could go to the state in taxes.

So, it's wise to look into these matters sooner rather than later to save a significant amount of money.

Like I talked about with my student's mom's story, trusting financial advisors without checking in can lead to no growth and high fees.

It's all about making sure our parents' hard-earned money is taken care of the right way!

So, note down these 3 steps to help your parents protect their money:

1. Review Their Investment Portfolio: Understand where their money is invested and compare returns to market benchmarks.

2. Calculate Their Retirement Needs: Determine how much income they’ll need from their investments

3. Plan to Minimize Inheritance Taxes: Set up their finances early to reduce tax burdens, preserving more of their wealth for emergencies or inheritance.